On January 11th, 2022, Citigroup Inc ($C) filed an 8-K form with the SEC to notify its investors of its intention to “exit the consumer, small business and middle market banking operations of Citibanamex”. The name under which Citibank operates in Mexico.

The announcement shocked Mexico, and even though Citi had been losing market share in the Mexican banking consumer market for the past few years, no one expected this sudden retreat.

DYCSI experts believe that this event will bring big changes to the banking landscape in Mexico. The impacts will be perceived in the financial market itself, but will also reach the IT sector, especially professionals and companies providing services in the financial industry. However, the exit process could take more than a year to be completed.

“I think that an agreement might be closed by the end of the year, and another 6 months will be needed to fully get all the regulatory approvals from both the Mexican and American authorities.” —Jose L. Torres Vivanco, President of the Board of Directors

Is Mexico the only one affected?

No. On April 15th, 2021, Forbes reported Citi’s intentions to exit retail banking in 13 countries. However, these 13 countries were mostly Asian: Australia, Bahrain, China, India, Indonesia, Korea, Malaysia, the Philippines, Poland, Russia, Taiwan, Thailand, and Vietnam. Mexico was not on this list.

The exit process for these other countries has also started, as Reuters reported on January 13th, 2022, that a $3.65 billion USD agreement between Citigroup and the United Overseas Bank (UOB) has been reached to sell its consumer business. The sale includes operations in Indonesia, Malaysia, Thailand, and Vietnam. Achieving the goal in 4 out of the 13 intended markets.

What happens next?

In Mexico, once the authorities provide the approval, the changes will start to flow according to the deals to be reached.

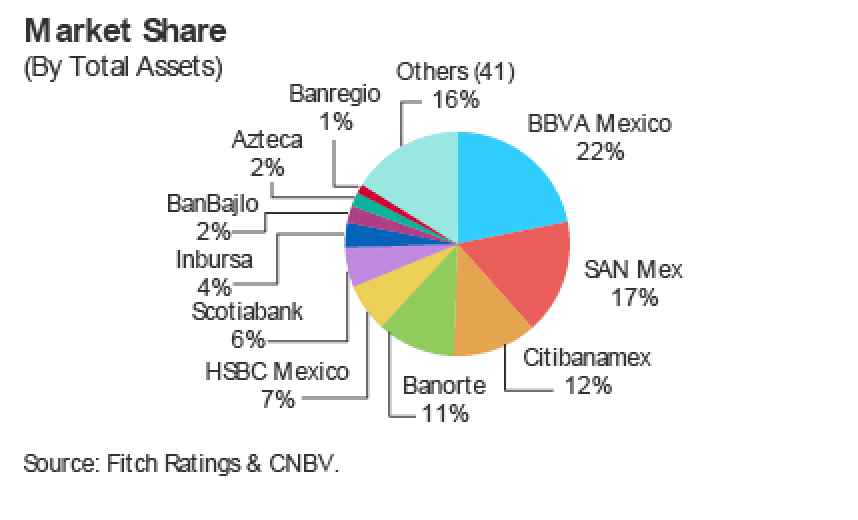

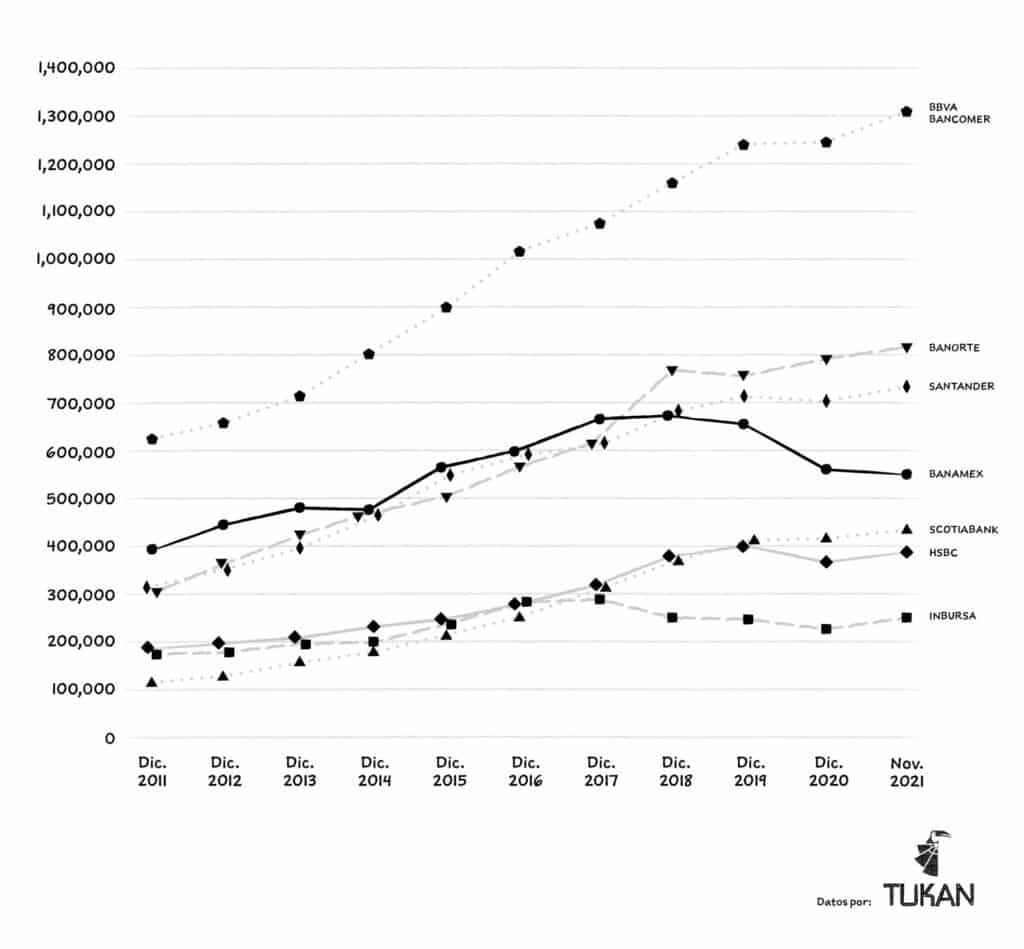

The buyer will have a fully-fledged bank 100% ready to operate. Given its size and reputation (Banamex, the Mexican bank that Citibank bought in May 2001 for $12.5 Billion), it will be the best approach to keep it working as-is and keep the brand to capitalize on customer’s loyalty to it.

If the buyer is a Mexican bank (Banorte $GFNORTEO.MX, Banco Inbursa $GFINBURO.MX or Banco Azteca PRIVATE), the most likely scenario is that they migrate their operations and IT infrastructure to the Banamex platform. Alternatively, they can adjust the market segmentation of banking products among bank brands. For example, Banorte bank might consolidate their retail banking operation in Banamex’s platform and keep their upper market operations in their current systems.

From what we know, Citi’s tech platform was developed and maintained via outsourcing from India, with IT designers and architects in the USA. Additional IT teams per market to localize the solution are also in place. In Mexico in particular, the Banamex in-house IT team is numerous, and many outsourcing vendors also provide services bringing even more people to the picture.

Banamex’s IT primary and secondary teams should not be worried though, because in any case, they are the ones with greater knowledge of the solution, and new changes will have to be implemented to either migrate or adapt the solution going forward. In fact, it is more likely that Banamex will have to expand its IT team in the form of employees or vendors.

Is this because of Fintechs?

NuBank $NU –and we can infer that the Softbank fund as well— has denied interest in buying Banamex. However, this fintech company is already providing financial services in México (it bought Sofipo Akala in September 2021), and is not the only big-name gaining market share in the highly “unbancarized” Mexican population. Brands such as Hey Banco, Konfio, albo, and Klar are also growing their customer base each day.

This brings a question to mind. Are retail banking markets better served by fintechs and digital banks? One thing we can say for sure is that for Citi to compete in this market and regain the lost market share, relevant investments in digital banking solutions must be made. However, Citi’s revenue trend worldwide has seen a decline, and in this situation, it is hard to double down on this segment.

We will keep an eye on traditional brick-and-mortar banking institutions because the game is far from over and the virtual and digital solutions are only getting better. This might not be the last bank to make bold decisions in the retail banking segment.

This can also be good news for core banking solutions such as SAP C4B owned by SAP Fioneer, there might be new opportunities to renew core banking backend software.

For now, all we know is that Citi is exiting the lower and middle markets, and Banamex is up for sale. A big change in Mexico’s and the world’s financial industry has already started; an estimated transaction between 12.5 and 16 billion USD in Mexico, 3.65 billion USD already settled in Asia, and counting.

The outcome of this event will continue to generate news in the coming months.